Snapshot

A mirror for an Indian family’s financial life.

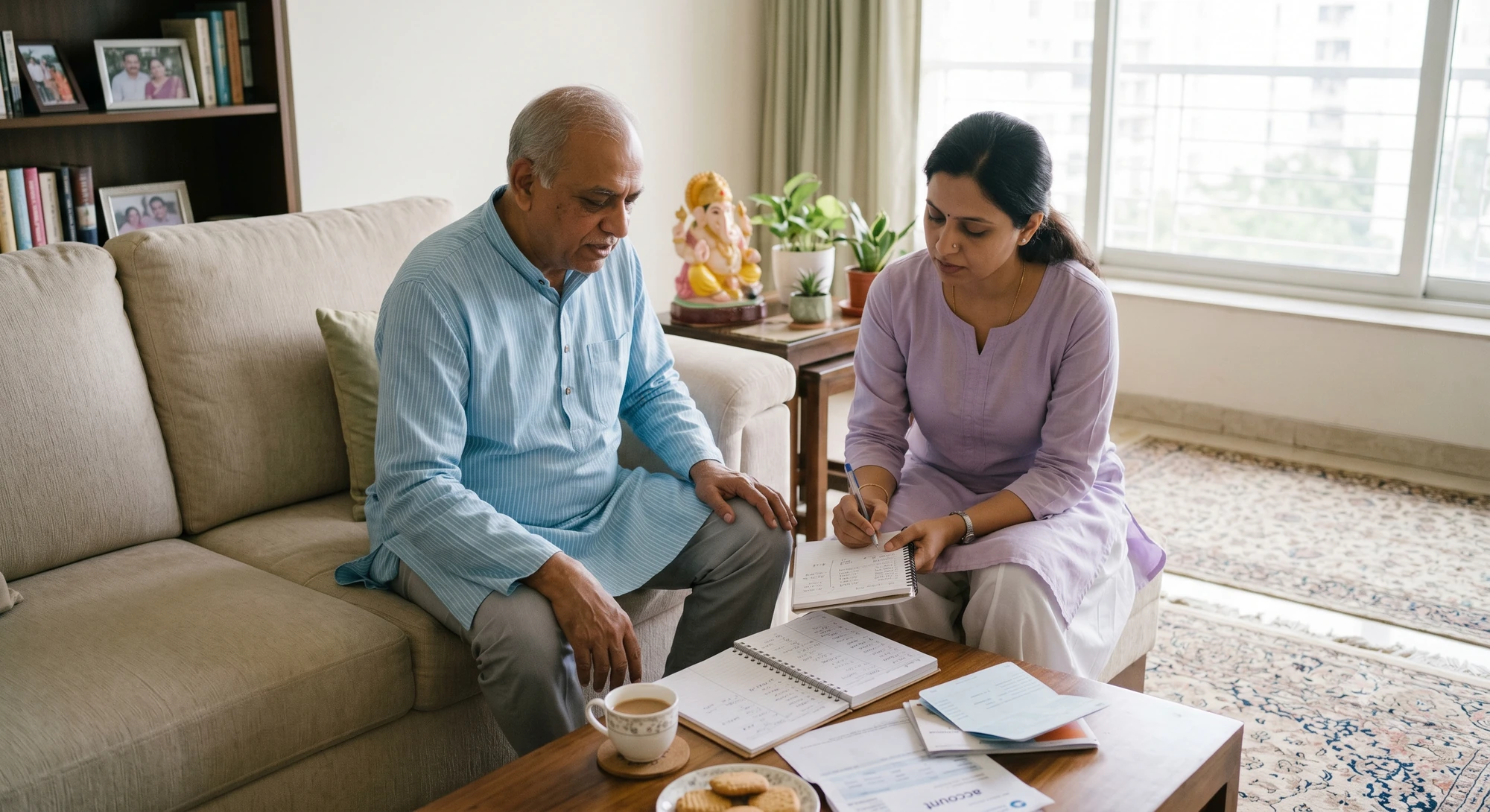

A Sunday afternoon. A daughter sits with her aging father, writing down every account he owns, having the difficult conversation while it is still possible. That is the product I helped design.

FOLO is a NetWorth app for Indian families, one place for everything they own and owe. The design problem was not features. It was trust, consent, comprehension, and emotional safety.

The problem

Most Indian families have no shared view of their financial life. The information exists, scattered across passbooks, forgotten logins, and paper in a drawer only one person knows about.

The cost surfaces at the worst moment. When someone passes away, the family searches under stress. Some assets show up in weeks. Many are never found. That “never found” is a measured number: in October 2025 the Finance Ministry put unclaimed financial assets at ₹1.84 lakh crore and launched a national campaign to return them (Business Standard).

- ₹78,213 crore in unclaimed bank deposits at the end of March 2024, up 26 percent in a year (RBI Annual Report).

- Close to ₹89,000 crore of shares parked with the Investor Education and Protection Fund, across 1,671 listed companies (IEPFA).

- ₹20,062 crore of unclaimed amounts with life insurers at the end of FY24 (IRDAI).

- ₹8,505 crore in 21.5 lakh inoperative EPF accounts, a fivefold rise in six years (Parliament reply).

Every rupee has an heir. What is missing is a single living record of a family’s money, built while everyone is still around to explain it.

India had quietly built the rails: Aadhaar for identity, UPI for movement, the Account Aggregator framework for consent, cheap data putting a smartphone in nearly every hand. The rails were ready. The product a family could actually use was not.

How I came to design FOLO

Sharpener Design joined Finuture Technologies in May 2023 to make finance simple for the god fearing government fearing citizen. The question that pulled me in: how can Indian families organise, manage, grow and share their NetWorth? That felt worth spending years on.

Munmun Desai brought the financial depth and founder conviction, Vishal Purohit the systems mind to make something this complex work. My job was to turn that ambition into a product language people could trust. The early Figma prototypes anchored the ₹10 Crore seed round. The initial idea was finance made simpler for women, but finance does not have a gender and everyone struggles, so FOLO became for one and all.

The design thesis

Open most finance apps and you meet the same room: cards on cards, graphs climbing and falling, a number competing for attention. Fintech design rewards the person who checks ten times a day.

FOLO refused that posture. The user was not coming to transact. They were coming to ask one quiet question: how am I doing? Net worth is the slow arithmetic of a life, what you own minus what you owe. It deserved a calm instrument, not another dashboard.

We graded all ninety screens on two numbers of our own, an easy score for whether it worked and a wow score for whether it felt like anything. Nothing shipped soft. The discipline was the thesis: a finance product earns trust by being quiet and exact.

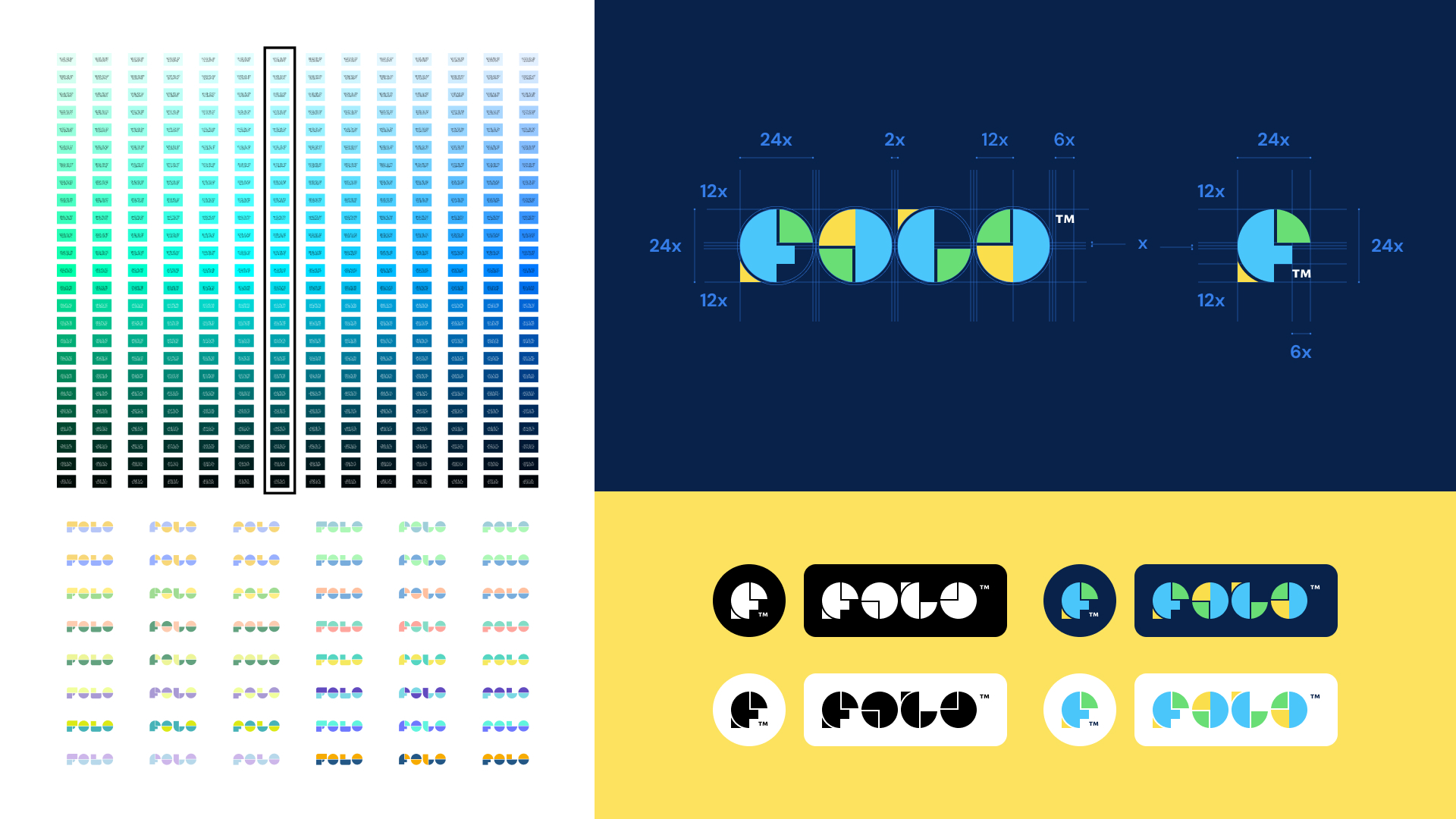

The brand

FOLO is an acronym before it is a name: Family Of Loved Ones. The whole product follows from that. The line we wrote early still holds the thesis: you know your worth of all you own and all you owe, you share your worth with those who are your own, and you forward your worth to the generations who will treasure it as their own. Own, share, forward.

Every decision was tested against four words: Friendly, Useful, Safe, Eternal. In the writing they became one voice, friendly, simple, warm, assuring, responsible.

The logo began as an F drawn from bars and arrows reaching for growth. It landed somewhere gentler: a wordmark of rounded petal forms in the system’s own blue, green, and yellow, so the brand carries the same colour meanings as the product. The display face is Ysabeau Infant, humanist enough that large numbers read as composed rather than clinical. Underneath it all, one line: net worth signifies security, freedom, and the pursuit of a better life. A child could help a parent use it. A parent could trust it enough to share.

The colour system

Blue carries assets. Yellow stands for liabilities. Green holds insurance. Indigo is the interaction colour, the stamp ink an Indian user already reads as authority. The product says it out loud: as the accounts connect, onboarding paints the screen blue.

Each hue was drawn into a full tonal ramp and carried everywhere, from the net worth screen to the certificate. The language is learned once and never relearned.

The primary screen: no graphs

The hardest decision was keeping graphs off the net worth screen. We explored charts, bars, dashboards, ratios. Most made the user work for an answer they wanted instantly.

So the screen became brutally simple. A large net worth numeral, a blue field for assets above, a yellow field for liabilities below, a calm greeting. Nothing else. The ratio of blue to yellow gives the position at a glance. Instead of reading a graph, the user feels the balance.

The category pages held the same restraint: one strong number, one plain sentence, a clear list. A finance product does not get smarter by showing more. It gets smarter by knowing what to leave out.

Onboarding: from a dot to a decimal

The first run opens on a single dot. It grows, splits, takes on green and then yellow, and settles into the net worth number as its decimal point. Your scattered financial life resolving into one figure.

For many people this is the first time they see their whole financial life as a single number, so the motion softens it rather than performs. Around it, a nudge engine kept people moving with encouragement instead of demands. “Only one in three people track their finances, you are already ahead.” Titles under forty characters, nudges under a hundred and fifty, so warmth never turned into noise.

Designing trust through consent

FOLO connects the most sensitive data a person has, so trust could not live in a privacy policy. It had to live in the interface. SEBI regulated, operating as a Financial Information User, AES-256 encrypted, connected through the RBI Account Aggregator framework via Finvu, MF Central, and EPFO, across five hundred plus institutions, and the product says so on the surface.

Consent was built as small, legible commitments rather than one heavy legal moment, and every flow carried its real states, not just the happy path. Sharing was never a quick tap. The copy rewrote itself with the selection: “Priya will see your Assets and Insurance.” A privacy setting, turned into a sentence about a person.

Account Health Check

Account Health Check scans connected accounts for the quiet cracks, nominee gaps, missing details, the things that become a family’s problem at the worst time. Building wealth matters, protecting it is essential.

The hard part was tone, because a health check can feel like an accusation. The line that carried it: “A nominee is your voice when you’re not there.” Precise enough for finance, human enough for family.

Where do I stand, and how am I doing

As the product matured it answered its two organising questions out loud. “Where do I stand?” became a sixty-second financial health check. “How am I doing?” became its forward-looking twin, each with quick calculators, short, plain, answerable in a sitting. This is where FOLO stopped being only a mirror and became an instrument for decisions.

The Timeline: planning the month ahead

The Timeline lays out the month’s upcoming outflows so a family can plan around what is due rather than be surprised by it. The hero screen’s philosophy applied to time instead of balance: show the one thing that matters, leave the rest out.

Community and FOLO Daily

FOLO Daily offers one small insight at a time. The community surface lets a real question rise, “I am buying a home worth two crore, what is the best way to fund it?”, and answers it with peer context. Used carelessly, benchmarking breeds anxiety, so the design job was making comparison feel like company rather than competition, with AI never sounding more confident than the product can defend.

LYNC: legacy planning

Legacy planning grew into a product of its own. LYNC is a human-led service that helps a family transfer a loved one’s assets after a loss, with dignity instead of a lost year. It is the part of FOLO I was most careful with, and it has its own story.

NetWorth Certificate

The NetWorth Certificate turned the core value into a formal document for the moments people need proof of standing, a visa, a loan. The problem was credibility without theatre. The indigo seal carried the product’s authority cue into an artefact, calm, official, easy to read. It made FOLO feel less like a tracker and more like an institution.

Sharing net worth with family

Sharing net worth can reassure or it can wound. So the model was control and consequence: your Net Worth, your People. The sheet lets a user decide exactly what another person sees, each category in its semantic colour, the header rewriting itself with the selection. The commit is deliberately slower than a tap, because a sensitive action should never feel accidental.

The co-creator loop

Before launch, FOLO was shaped by a close community of early users, closer to co-creation than research. The most useful signals came from the moments they hesitated. One lesson kept returning: a technically correct handoff is not enough, the user needs to know where they are going and how they get back. That shaped the Account Aggregator experience, and later became Co-create FOLO inside the product. For a product like this, feedback is not a growth tactic. It is a trust mechanism.

The craft behind it

FOLO shipped as a system: twenty-two flows, ninety screens, three hundred and eighteen states, each graded on eight dimensions before it could ship. Three pillars, product, communication, brand, one locked language underneath. The rigour is invisible in the final product, which is the point.

Launch and traction

FOLO launched publicly on 21 March 2025 and crossed:

- One lakh plus downloads

- 4.5 App Store rating

- ₹15,000 crore plus connected personal wealth

- Roughly 85 percent completion on the optimised onboarding flow

The traction came from giving people a clean view of something they already cared about and had never been able to see.

What still needs work

The product is young. The commentary layer needs to grow more contextual across asset classes. The AI surface needs the same discipline as everything else, because in finance AI cannot sound more confident than it can defend. And coverage has to widen, more asset classes, more languages, less explanation.

What this taught me

FOLO settled something for me. Brand is what the product promises, product is whether the promise survives contact with reality. Every colour, word, and consent screen had to carry one idea: this is your family’s financial life, and it deserves care.

A country where families cannot see what they are worth needs more than financial infrastructure. It needs interfaces that make the invisible visible, language that lowers fear, and products that help difficult conversations happen earlier. It starts with one family on one quiet afternoon, finally seeing itself clearly. The next family follows.

FOLO is live

FOLO is on the App Store and Google Play, with the full story at folo.one. You can also find it on Instagram and LinkedIn.